Cost & Aid

Your dreams are within reach.

As a Mount Mary graduate, you’ll have the knowledge, confidence and leadership skills to shape the future. And we’re here to make sure nothing stands in the way. That’s why 100% of full-time, undergraduate Mount Mary students receive an academic scholarship or reduced tuition.

2024-2025 FAFSA CHANGES FEDERAL STUDENT LOANS RETURN TO REPAYMENT

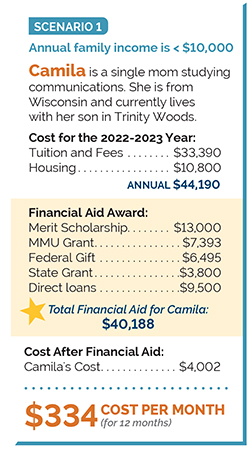

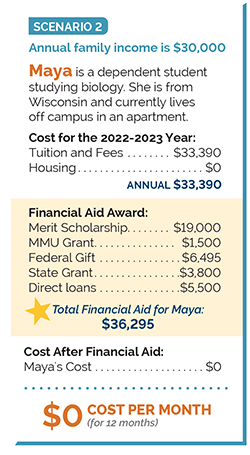

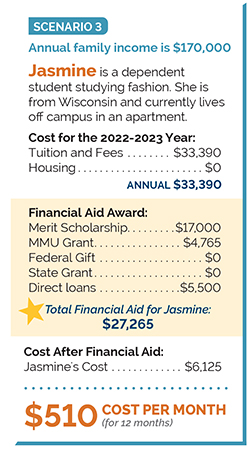

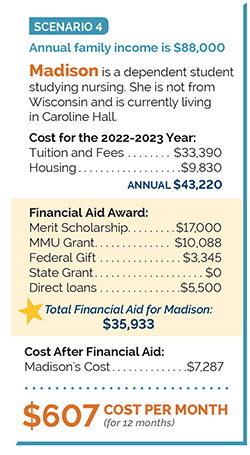

Mount Mary is affordable. Here are some scenarios to see how it can work for you.

Tuition and costs

The cost to attend a college or university for one academic year is called Cost of Attendance. It includes tuition for fall and spring semesters, fees, an estimate of average costs for books and supplies, housing and food, transportation, and personal expenses.

Making your education possible

Helping students and their families afford higher education is a top priority for us at Mount Mary University. To be considered for all financial aid, you need to submit the Free Application for Federal Student Aid (FAFSA). This form will determine your eligibility for federal, state, and institutional grants, loans, and work study. Mount Mary University's Federal School Code: 003869.

Look at the Financial Aid Timeline, including when you should apply for various scholarships, FAFSA, and other aid. We're here to help every step of the way.

Affordable payment plan options are available.

Coming from a low-income family, I worried that college would not be attainable. However, Mount Mary’s scholarships helped me not worry about the cost of tuition and place my entire focus on my education.

Suanet Negron-Valdez ‘19, Spanish & Biology Major

Scholarships & Financial Aid

An academic scholarship is just a starting point for the financial assistance available. More than 90% of students also benefit from additional financial aid programs including grants, loans and campus employment opportunities.

Scholarship programs

Mount Mary offers three unique, four-year scholarship opportunities for first-year, full-time undergraduate students. The programs provide Scholars with academic, professional and financial support through a group learning model that encourages community building and leadership development.

As a Scholar you will:

- receive one-on-one advising and peer mentoring

- receive Scholar program based academic, social, mental health, and financial support through various campus resources

- receive monthly professional development opportunities to assist with post-graduate preparation

- belong to a sisterhood that supports relationship-building and a sense of community

CAROLINE SCHOLARS PROGRAM

Award: Full tuition and standard room and board

Eligibility: Full-time incoming undergraduates with a minimum 3.5 cumulative high school GPA who demonstrate a passion for social justice.

Grace Scholars Program

Award: 85% of tuition

Eligibility: Full-time incoming undergraduates from the city of Milwaukee or city of West Milwaukee who demonstrate leadership skills and have financial need.

Jewel Scholars Program

Award: $26,000-27,000 per year

Eligibility: Full-time incoming undergraduates and transfer students with a minimum 3.0 cumulative GPA who are STEM majors

Frequently asked questions

Our Financial Aid Office has compiled a list of common questions many prospective students have throughout the financial aid process. If you have additional questions, please contact your admission counselor and she will be happy to help.

Financial aid encompasses loans, grants, scholarships, and work-study employment opportunities—all are forms of money to help pay for college.

You must complete the Free Application for Federal Student Aid (FAFSA) form to be considered for federal, state, and institutional grants and loans, as well as for some scholarships. You need to complete the FAFSA each year. Learn more about how to apply for financial aid.

Mount Mary’s FAFSA code is: 003869. Please enter this code in the School Code section of the FAFSA.

Mount Mary offers several on campus housing and meal options. Room and board rates vary depending on the type of room you prefer. View room and board rates.

Mount Mary awards an academic scholarship to nearly every full-time incoming undergraduate first year and transfer students upon acceptance to the university. Additional Mount Mary scholarships are available based on review of data submitted in the FAFSA. Learn more about scholarships at Mount Mary.

For undergraduates, it is important to apply for scholarships during your senior year of high school or at least one term before enrolling at Mount Mary. For scholarships at Mount Mary, most scholarship deadlines occur between December and February each year. Mount Mary academic scholarships do not require an application; they are awarded automatically to eligible students upon acceptance to the university.

For graduate students, most scholarship deadlines occur between June and September.

Eexternal organizations (community organizations, foundations, employers, professional organizations, etc.) may allow you to apply for scholarships prior to your senior year of high school. We encourage you to look for scholarships early—even as early as your sophomore or junior year—so you can take advantage of those opportunities and plan for deadlines.

To be considered for grant or loan programs, you must file the Free Application for Federal Student Aid (FAFSA). Learn more about how to apply for financial aid.

Mount Mary offers a way to obtain an estimate of the financial aid you may be eligible to receive using our Net Price Calculator. This option is for first-year or transfer undergraduate students only.

To receive your financial aid offer, you must be accepted at Mount Mary and have completed the FAFSA. Please make sure to enter Mount Mary’s school code so that we receive your FAFSA information. New students for Fall 2024 can expect to receive their offers in February 2024. Continuing students in March of 2024.

Log in to your MyMountMary account and select the Finances tab. Select MyFinancialAid to accept or decline your awards and complete any necessary documents. See more information about what to do after filing for financial aid.

Loans and scholarships are disbursed to your account as soon as possible after all information is received and processed and the term has started. Contact the Business Office with questions about your tuition bill. If you need to set up a payment plan, log in to your MyMountMary portal and click on the Finances tab. You will see Transact Payments which is the payment plan provider, or you may also contact the Business Office.

Our admissions team is here to help

The best way to get started is to get in touch. We’ll answer your questions, help you explore programs and walk you through the admissions and financial aid process.